US Lifts Restrictions on Anthropic’s Powerful AI Models Fable and Mythos

July 1, 2026

The Shocking New Numbers Behind Apple’s Mammoth iPhone 18 Pro Max Battery Leak

July 3, 2026

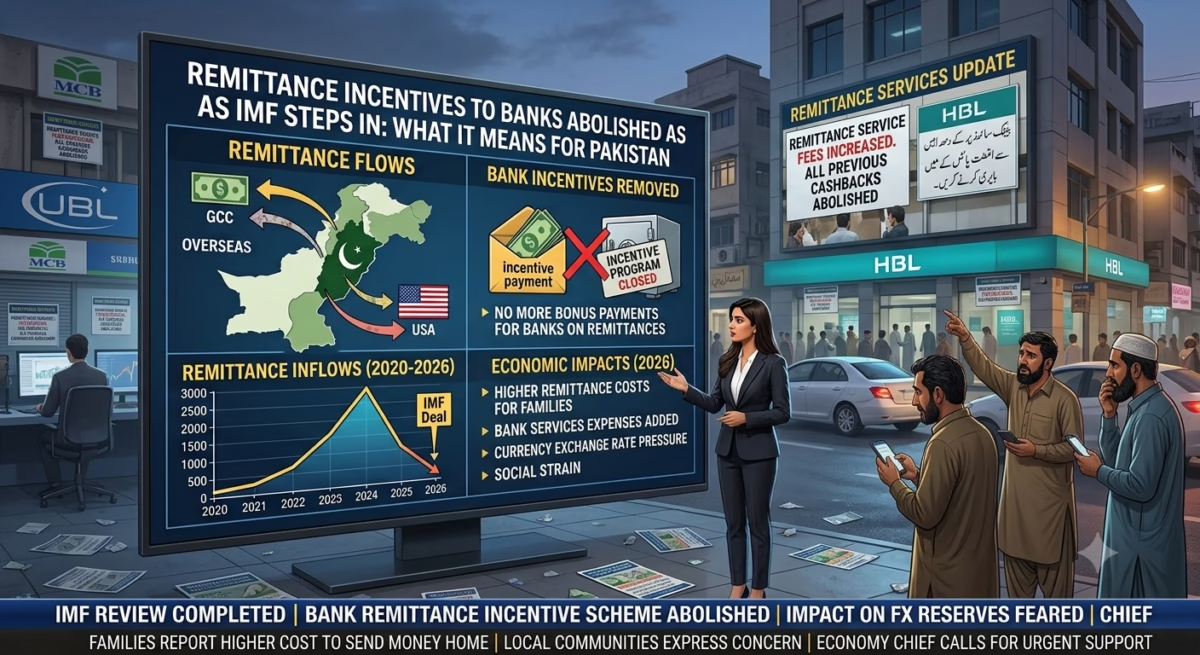

Remittance Incentives to Banks Abolished as IMF Steps In

Pakistan has officially ended two major incentive schemes designed to encourage banks and overseas Pakistanis to use formal remittance channels. The decision, announced by the State Bank of Pakistan (SBP), comes after concerns raised during discussions with the International Monetary Fund (IMF) over the growing fiscal cost of these programs.

The move marks a significant policy shift in Pakistan’s remittance strategy. While financial incentives for banks have been abolished, the government says overseas Pakistanis will continue to enjoy free remittance services through authorized banking channels.

What Changed?

The SBP has discontinued two key schemes effective from July 1, 2026:

- Sohni Dharti Remittance Programme (SDRP), which rewarded overseas Pakistanis with redeemable points for sending money through formal channels.

- Telegraphic Transfer Charges Incentive Scheme (TTCIS), under which banks received reimbursements for keeping remittance transfers free for customers.

Although no new rewards will be issued under SDRP, points earned before June 30, 2026, will remain redeemable until June 30, 2027.

Why Did the IMF Step In?

According to reports, the IMF questioned the rising cost of these incentive programs, particularly the TTCIS, which had become a significant financial burden on the national budget.

Industry estimates suggest the annual cost of the transfer charge reimbursement scheme had grown substantially, prompting calls for fiscal reforms and more efficient use of public funds.

The IMF reportedly viewed these subsidies as unnecessary now that Pakistan’s formal remittance system has matured and digital money transfer services have become more efficient.

What Is a Remittance Rebate?

A remittance rebate is a financial incentive offered to encourage overseas workers to send money through official banking channels.

Such incentives may include:

- Reward points

- Cashback offers

- Reduced transaction fees

- Free money transfer services

- Loyalty benefits

Pakistan introduced these measures to increase documented foreign exchange inflows and discourage informal money transfer networks.

Will Overseas Pakistanis Still Send Money?

Experts believe remittances are likely to remain strong despite the removal of these incentives.

Several factors continue to support inflows:

- A growing number of Pakistanis working abroad

- Increased use of digital banking

- Faster international money transfer services

- Greater trust in formal financial channels

Industry representatives expect Pakistan to remain on track for strong remittance growth in the current fiscal year.

Remittances and Pakistan’s Economy

Workers’ remittances play a crucial role in Pakistan’s economy.

They help:

- Strengthen foreign exchange reserves

- Support the Pakistani rupee

- Reduce the current account deficit

- Finance imports

- Increase household incomes

- Boost domestic consumption

In recent years, remittances have become one of Pakistan’s largest and most stable sources of foreign exchange.

Have Remittances Increased?

Yes. Pakistan has witnessed record remittance inflows in recent years as more overseas Pakistanis use official banking channels.

Higher employment abroad, improved banking infrastructure, and digital payment solutions have all contributed to this upward trend.

Government Initiatives to Attract Foreign Remittances

Over the years, Pakistan introduced several initiatives to encourage overseas Pakistanis to send money through banks.

These included:

- Reward programs

- Free transfer services

- Mobile applications

- Partnerships with international money transfer operators

- Digital banking improvements

While some incentive programs have now ended, the government says it remains committed to maintaining efficient and low-cost remittance services.

Remittances in FY23 and Beyond

Remittance inflows have remained resilient over the past several fiscal years despite global economic uncertainty.

Strong contributions from overseas Pakistanis have helped stabilize the country’s external account, making remittances one of the most reliable pillars of Pakistan’s economy.

Officials believe this trend can continue even without direct financial incentives for banks.

Is Remittance Based on a Shariah Concept?

In Islamic finance, remittances are generally associated with the concept of Hawala in its original lawful sense of transferring debt or financial obligations. Modern banking remittances processed through regulated financial institutions are also considered permissible, provided they comply with Islamic financial principles and avoid prohibited elements such as interest (riba).

Islamic banks often facilitate remittance services through Shariah-compliant banking products to ensure transactions meet Islamic ethical standards.

Impact on Banks

Commercial banks will no longer receive government reimbursements under the discontinued incentive schemes.

However, the SBP has instructed authorized dealers to continue providing qualifying home remittance services without charging fees to senders or beneficiaries, preserving a key benefit for overseas Pakistanis.

Challenges Ahead

Despite strong remittance performance, Pakistan still faces several challenges:

- Exchange rate volatility

- Global economic uncertainty

- Competition from informal transfer channels

- Rising compliance costs

- Maintaining confidence among overseas workers

Addressing these issues will remain important for sustaining future remittance growth.

Future Outlook

Economists generally expect Pakistan’s remittance inflows to remain resilient despite the withdrawal of incentive schemes. Continued migration for overseas employment, expanding digital payment infrastructure, and established banking networks are expected to support formal inflows in the years ahead.

Conclusion

The abolition of remittance incentives for banks marks an important shift in Pakistan’s financial policy under IMF-backed reforms. While the government is ending costly subsidy programs such as the SDRP and TTCIS, it aims to preserve free remittance services for overseas Pakistanis and maintain strong inflows through formal banking channels. With remittances continuing to play a vital role in Pakistan’s economy, the success of this policy change will depend on sustained confidence among overseas workers and continued improvements in the country’s financial system.

Frequently Asked Questions (FAQs)

Why did Pakistan abolish remittance incentives?

The government ended the schemes as part of fiscal reforms after concerns over their growing cost were raised during IMF discussions.

What is the Sohni Dharti Remittance Programme (SDRP)?

It was a rewards program that offered redeemable points to overseas Pakistanis who sent money home through formal banking channels.

What is the Telegraphic Transfer Charges Incentive Scheme (TTCIS)?

It reimbursed banks for transfer charges so that remittance services could remain free for customers.

Will overseas Pakistanis still be able to send money for free?

Yes. The SBP has instructed authorized banks to continue offering eligible home remittance transfers free of charge.

How do remittances impact Pakistan’s economy?

Remittances strengthen foreign exchange reserves, support the rupee, finance imports, and provide income for millions of households.

Are remittances expected to decline after these changes?

Most industry experts believe remittance inflows will remain resilient due to strong overseas employment and well-established formal banking channels.

Elevate Your Brand with MasterInDesign

Don’t let your business get left behind in today’s fast-paced digital world. At MasterInDesign, we specialize in helping brands stand out, engage audiences, and grow online.

Take the next step toward digital excellence. Contact us today and transform your brand into a powerful online

{kind=link}

{kind=link}

{kind=link}